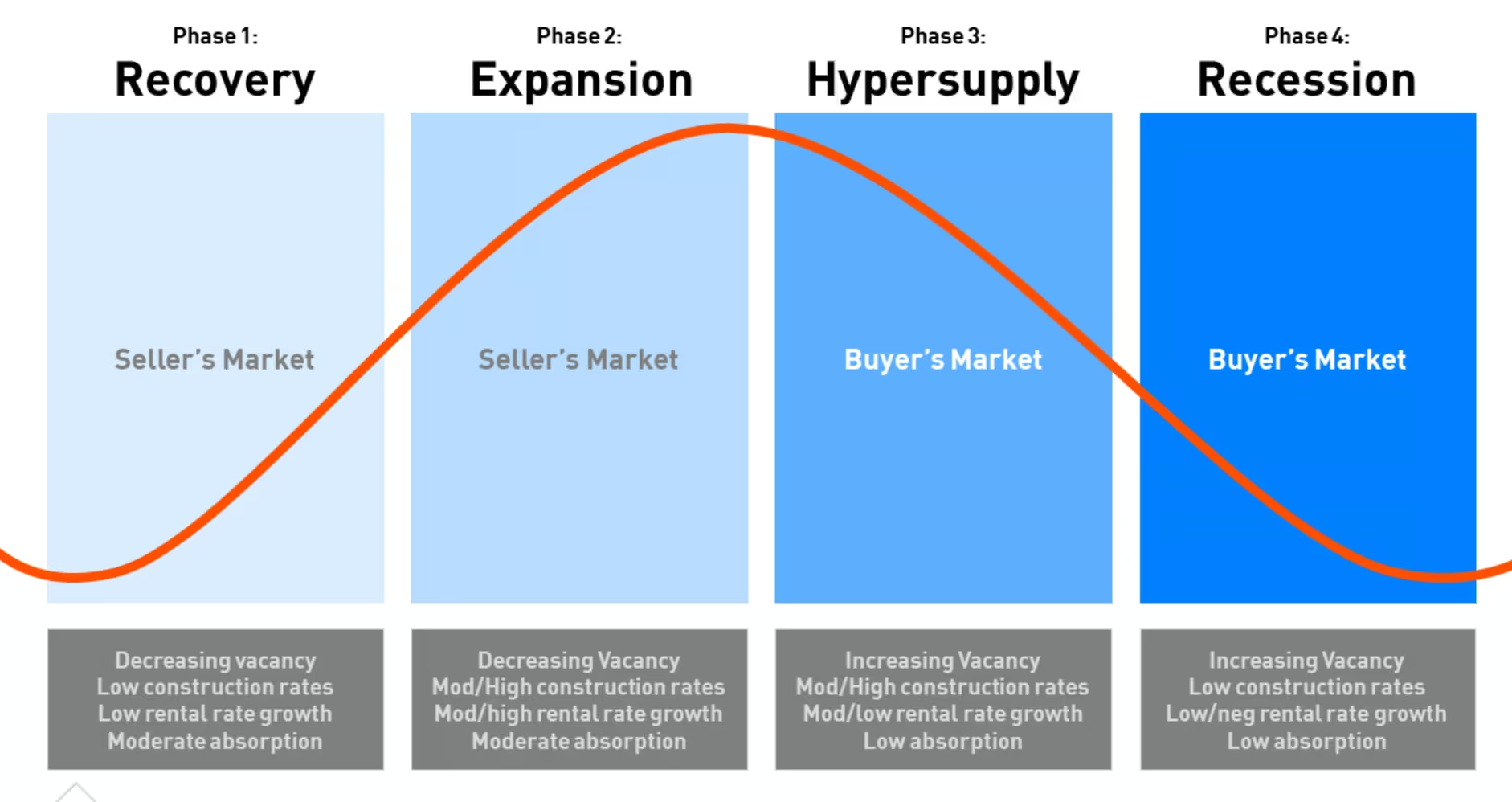

Real estate has always moved in cycles, a reality investors ignore at their peril. Most analysts divide the cycle into four distinct phases: Recovery, Expansion, Hyper-Supply, and Recession.

- Recovery begins after a downturn, when vacancies are high but new construction has slowed and early investors recognize value opportunities.

- Expansion follows, as demand strengthens, rents rise, and new development accelerates.

- Hyper-Supply occurs when optimism leads to overbuilding, supply overtakes demand, and vacancies begin to climb.

- Recession is the correction stage, where rents flatten or decline, values drop, and distressed sales create new entry points for the next wave of investors.

These cycles, documented by researchers such as Glenn Mueller in the Journal of Real Estate Portfolio Management and tracked by institutions like the Urban Land Institute (ULI), have repeated for decades with striking consistency. Knowing where we are in the cycle is often more important than the property type or market chosen.

The Current Context: Cyclical Headwinds and Emerging Opportunities

Real estate investing is inherently cyclical, marked by periods of growth, challenge, and opportunity. In recent years, investors and sponsors—including Camino Verde Group—have navigated both the highs and lows of this reality. Elevated interest rates, surging insurance costs, and tighter capital markets have pressured many projects. Some have outperformed expectations, while others have faced losses.

These challenges underscore a timeless truth: downturns often lay the groundwork for the next wave of opportunities. Today, signs suggest we are nearing the bottom of the current cycle—a historically favorable entry point.

Why Now May Be a Pivotal Moment

Cyclical Lows Create a Unique Entry Point

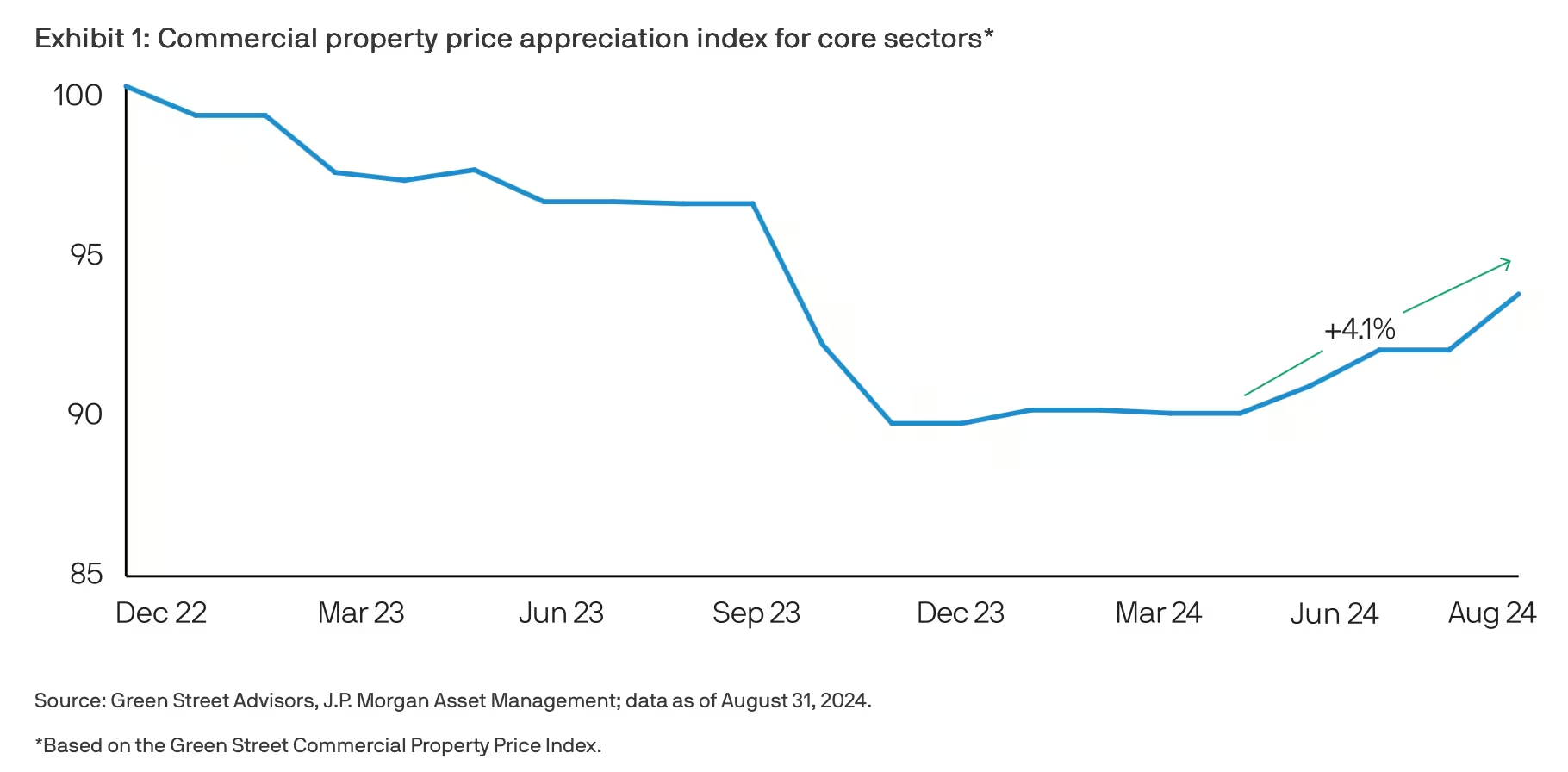

Commercial real estate prices have fallen sharply since their 2022 peak. J.P. Morgan estimates that values are down 24% from highs, but recent transaction data shows prices recovering by 4.1% in recent months. Historically, buying during such periods of correction has led to some of the strongest generational returns, as cap rates compress, occupancies remain stable, and net operating income (NOI) continues to grow.

A More Favorable Interest Rate Environment

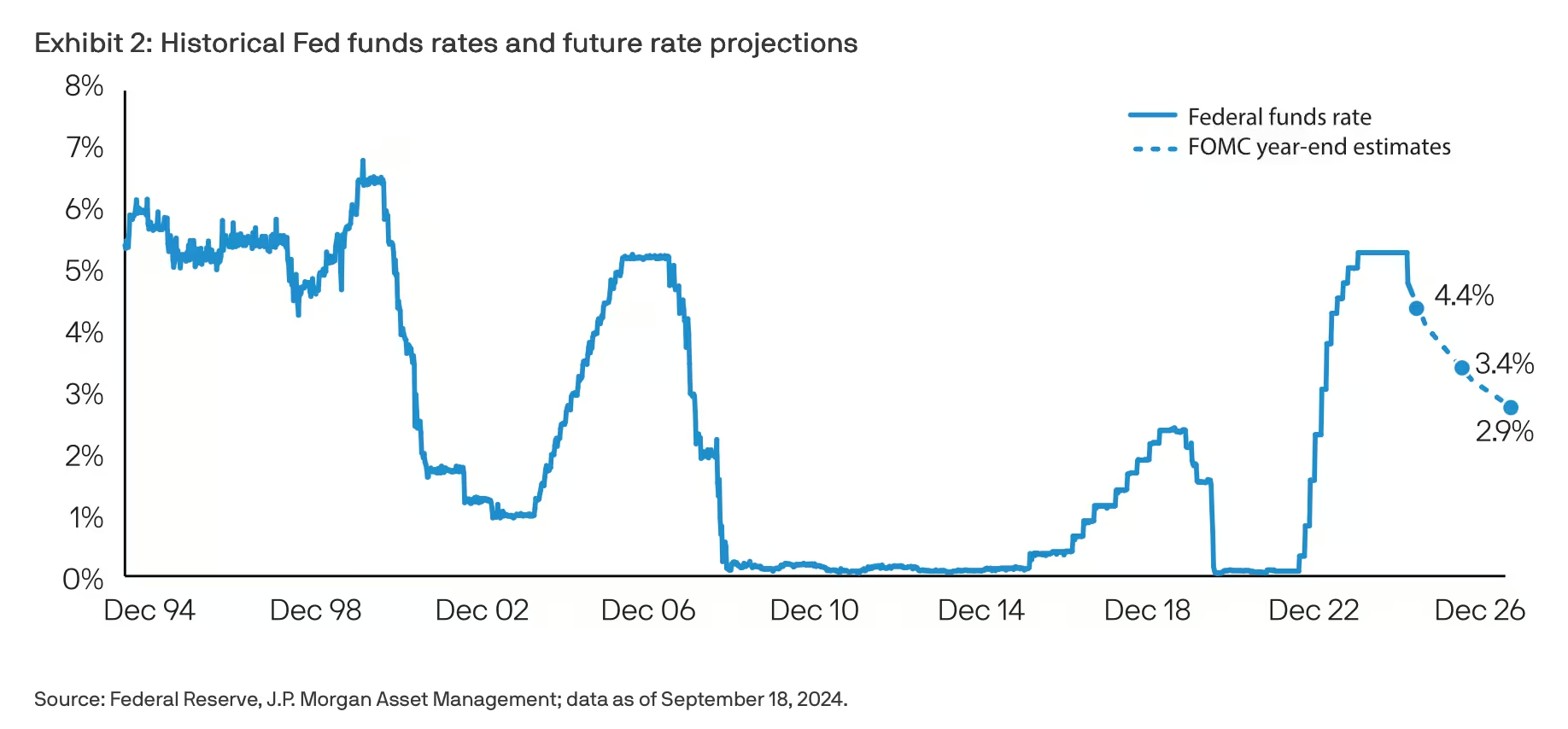

The Federal Reserve has signaled it is nearing a pivot from aggressive tightening to potential easing. Markets currently anticipate rate cuts in late 2025, a move that would reduce borrowing costs for acquisitions and development. According to CME FedWatch, futures markets recently placed the probability of a FED rate cut this week at over 95%. Lower rates improve debt service coverage, expand buyer pools, and ultimately lift valuations.

Strong Structural Tailwinds

Beyond monetary policy, real estate fundamentals are turning favorable. Construction starts are declining due to financing challenges, limiting future supply. Meanwhile, housing demand—especially for multifamily rentals—remains resilient, fueled by demographic growth, affordability challenges in homeownership, and urban-to-suburban migration patterns. Liquidity is also returning as private-credit providers step into gaps left by cautious traditional lenders.

Real Estate as a Long-Term Inflation Hedge

Despite short-term volatility, real estate has historically provided a strong hedge against inflation. Rents and property values tend to rise alongside broader price increases. While the Consumer Price Index (CPI) has cooled in recent months, the Producer Price Index (PPI) suggests potential cost pressures ahead. For investors, this translates into higher replacement costs and rental income growth, preserving long-term asset value.

Alternatives Enhance Portfolio Resilience

Institutional research, including from BlackRock and Preqin, highlights that private real estate offers low correlation to equities and bonds. In volatile market conditions, this diversification is increasingly attractive. Institutional allocations to private real estate remain robust, signaling confidence in the sector’s long-term role in balanced portfolios.

Signs of Investor Re-Engagement

Capital is beginning to flow back into the sector. Blackstone, for example, has re-entered select office and multifamily acquisitions, betting on long-term recovery. Private-credit funds are also actively providing bridge and mezzanine financing, filling a crucial role in transactions slowed by bank retrenchment. Renewed liquidity supports price stabilization and sets the stage for renewed transaction momentum.

Our Strategy: Disciplined, Opportunistic, Balanced

At Camino Verde Group, we approach this moment with clarity and discipline. Our strategy is built on four pillars:

- Short-Term Vigilance: Proactively managing underperforming assets to stabilize and maximize value.

- Selective Deployment: Pursuing only opportunities that meet rigorous underwriting standards and demonstrate significant value-add potential.

- Long-Term Perspective: Maintaining a five- to seven-year horizon to capture appreciation and ride out interim volatility.

- Risk Awareness: Acknowledging current market challenges while positioning to capitalize on tomorrow’s growth.

Closing Thoughts

The recent cycle has tested both sponsors and investors, a reminder that real estate is never static. Yet history shows that downturns often precede the strongest recoveries. With interest rates poised to decline, fundamentals strengthening, and capital beginning to re-engage, we believe this is a pivotal time to act.

At Camino Verde Group, we remain committed to navigating this cycle with clarity, prudence, and confidence—seeking opportunities aligned with market realities and designed to deliver sustainable, long-term success for our investors.